According to the Spring 2026 Industrial/Logistics Investor Outlook, investor mood is influenced by asset quality, location, and changing occupier needs, and the market is still fundamentally robust. When pricing industrial assets, investors carefully consider physical characteristics, tenant credit, lease structure, and long-term demand trends. As a result, capitalization rates continue to reflect a wide range of risk and return.

At the asset level, Class B and C properties offer better yields but necessitate more examination of functioning, condition, and tenant stability. Class A properties, which are distinguished by modern design, higher clear heights, and strong locations, continue to attract the most aggressive pricing. Investors are paying more attention to operational efficiency, accessibility to important transportation infrastructure, and proximity to labor and population centers across all asset types because these variables have a direct impact on tenant demand and long-term value.

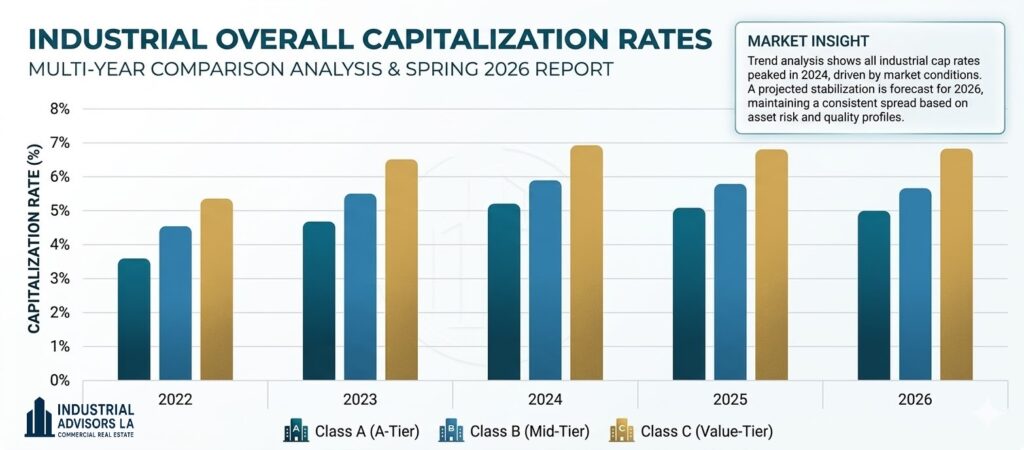

Industrial cap rates have essentially stabilized from the standpoint of the capital markets. The average cap rates for Class A, Class B, and Class C assets are roughly 5.28%, 6.02%, and 7.38%, respectively, with relatively slight year-over-year fluctuations. While ongoing instability in global economic conditions and policy remains a crucial watchpoint, investors anticipate interest rates to gradually decrease in the second half of 2026, which might somewhat compress cap rates, especially in core regions.

Strong industrial fundamentals continue to serve as the foundation for demand. Large-scale logistics customers drove a comeback in leasing activity in late 2025, with buildings larger than 500,000 square feet driving significant absorption. Occupiers are selecting less expensive interior markets over pricey coastal areas and combining into larger, more efficient Class A complexes. This change is maintaining demand for contemporary distribution space and strengthening build-to-suit development.

Industrial Real Estate Outlook Summary for 2026

Investor strategy is becoming more and more divided. While value-add investors are aiming for shorter lease terms and below-market rates to capture mark-to-market upside, core capital is still pursuing premium assets in significant distribution hubs. Although actual Class C demand is still low, infill locations close to densely populated areas are still in high demand, especially for resolving last-mile logistics issues. Additionally, buyers’ and sellers’ pricing expectations are aligning, which will sustain transaction activity until 2026.

The industrial sector’s long-term prospects are still very promising. Demand is anticipated to be sustained by limited new supply, increasing occupancy, and ongoing expansion in e-commerce, onshoring, and AI-driven supply chain efficiencies. Major distribution markets are expected to perform well, solidifying industrial as one of the most resilient and appealing asset classes in commercial real estate, even as investors continue to pay attention to interest rates, tariffs, and geopolitical threats.